Insurance for Community Groups, are you Suitably Covered?

There’s a whole range of insurance for community groups, and it can be tricky to get your head around the different types. Here is a straightforward guide to the types of insurance options available to community groups, and what each one covers against.

Trustee Indemnity Insurance For Community Groups

Regardless of good intent, trustees can be held liable for poor decisions or wrongful actions if they have caused a loss to the group. Trustee indemnity insurance covers the legal expenses of such claims and defends a trustee against disqualification, investigations or extradition proceedings. Trustees should give serious consideration to the cover; without it, should an allegation of mismanagement be made against them, they may have to defend the claim from their own personal wealth.

Professional Indemnity Insurance

This insurance covers your group against poor or negligent advice provided to its service users which has resulted in them suffering a financial loss. It’s generally considered essential cover if your group provides advice; for example offering counselling sessions. It covers the legal costs in defending the claim, as well as any compensation or damages payable to the claimant.

Public Liability Insurance

All community groups that deal with members of the public should consider taking out public liability insurance. It is a relatively inexpensive cover and protects against allegations of injury caused to a third party. This could be, for example, if someone was to trip over a loose wire at an event, or a kettle was knocked over and scalded a visitor.

Public liability insurance also covers against damage caused to third party property- this could be if carpets were irreparably damaged or walls badly marked after your group hired a premises. Most landlords or local authorities will require your group to have public liability insurance before allowing you to rent somewhere or hold an event.

Employers Liability Insurance

If your community group has employees, employers liability insurance is a legal requirement. It covers your group against allegations of injury or illness suffered by staff during their employment.

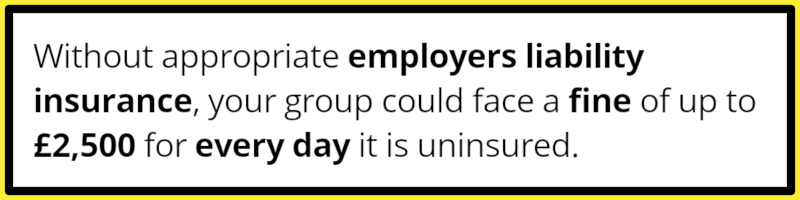

Without appropriate employers liability insurance, your group could face a fine of up to £2,500 for every day it is uninsured. Most insurers also cover your group’s volunteers under employers liability insurance, however some insurers may cover volunteers under public liability insurance. If you’re unsure which cover they are insured under, check your policy, wording or speak to to your insurer/ broker.

Property Damage Insurance

If your groups owns a building, this insurance covers your building against fire, theft, flood and other disasters, as well as its contents- such as stock and computer equipment.

Insurance for community groups

As we have identified above, insurance for community groups is absolutely essential as your group could potentially be exposed without the correct cover in place. But where do you start and what do you need? Contact us now and let our friendly team of community group insurance specialists help you make the right choice so your group is protected.

To read more about successfully insuring & planning a fundraising event check out our previous blog.

For more tips and tricks on all things related to charities, not-for-profits and community groups, follow us on Facebook, Twitter & LinkedIn.